North Midlands Credit Union have partnered with the Strategic Banking Corporation of Ireland (SBCI) to bring you the Home Energy Upgrade Loan Scheme (HEULS).

The scheme supports energy efficiency and renewable energy upgrades where those works are also being grant-aided by the Sustainable Energy Authority of Ireland (SEAI)

Whether you’re looking to make your home warmer, increase your Building Energy Rating (BER), reduce your energy bills or contribute to a greener environment – we have a lower rate loan option that could suit you!

Am I Eligible for the SBCI Home Energy Upgrade Loan Scheme?

This scheme is open to new and existing NMCU members that are undertaking home energy upgrades using a Sustainable Energy Authority of Ireland (SEAI) registered One Stop Shop or Community Project Co-ordinator.

The first step is to confirm that your home and improvement plans fit the eligibility criteria. The loan is for private homeowners in Ireland (including rental properties). Mixed-Use Property, Short-Term Lettings and Holiday Homes do not qualify.

Loan Purposes

Loans must be used for the purposes of upgrading the energy efficiency and decarbonisation of a qualifying residential properties.

- 75% of the loan needs to be for eligible energy efficiency purposes (e.g. insulation) and/or renewable energy solutions (e.g. heat pumps).

- Up to 25% of a loan may be applied for ancillary expenses, excluding financing any form of fossil fuel boilers.

- The upgrades need to result in at least a 20% improvement in your home’s energy efficiency, your SEAI registered One Stop Shop, Energy Partner, or Community Project Co-ordinator will assess this for you.

- You can apply for SBCI Home Energy Upgrade loans in respect of up to a maximum of three relevant residential properties.

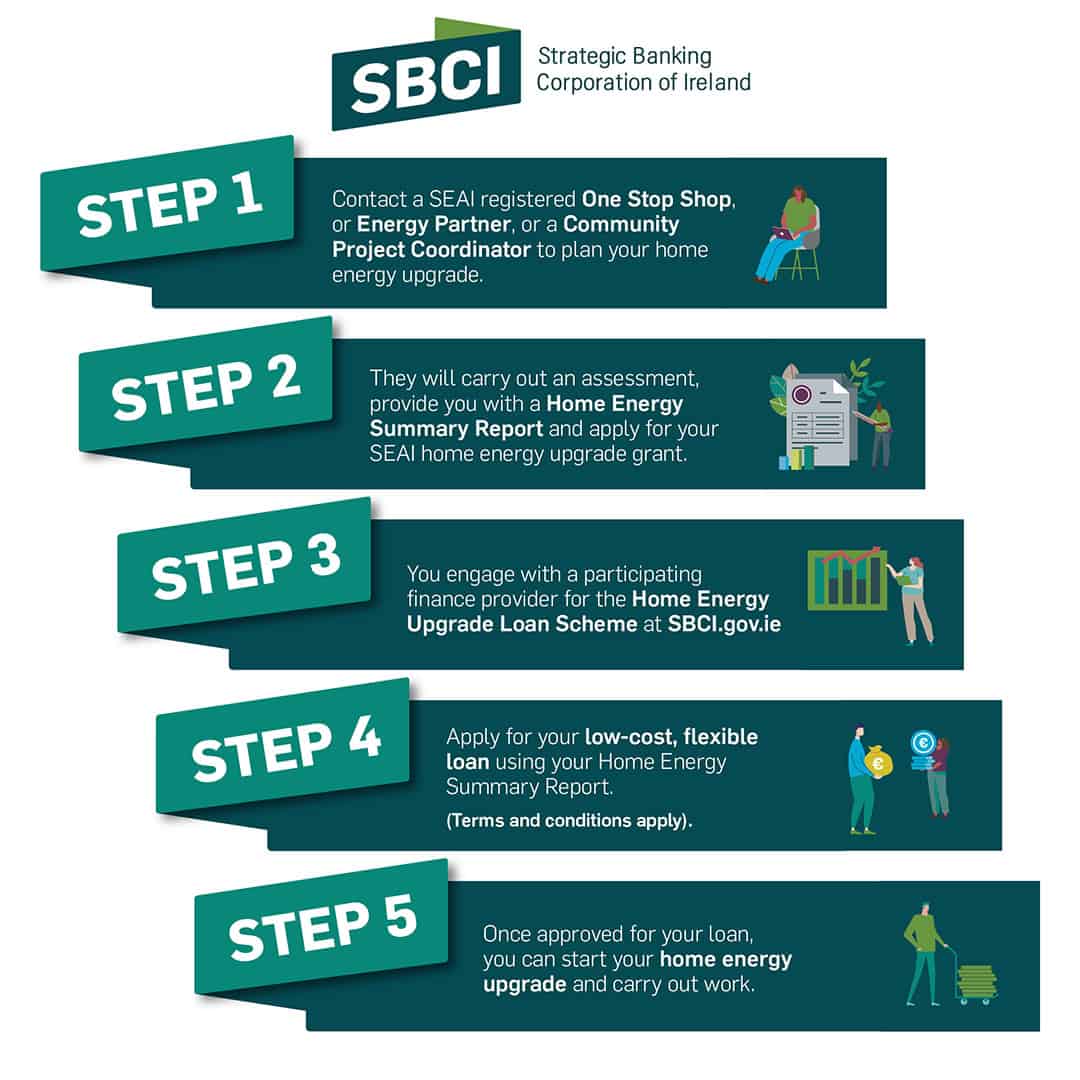

If you think you meet the above criteria then to start your journey, you need to engage with an SEAI registered One Stop Shop, Energy Partner, or Community Project Co-ordinator and have a home energy assessment completed before applying for the loan.

Applications that do not meet the SBCI Eligibility criteria will be identified prior to submission and will not proceed.

Loan Features

-

Affordable Financing

Unsecured loans from a minimum of €5,000 to a maximum of €75,000 per property – maximum aggregate loan of €225,000 per applicant if borrowing for more than one property (maximum three properties).

-

Flexible Terms

Choose a loan term that works for you – from a minimum of one year to a maximum of 10 years. Paying weekly, fortnightly or monthly.

-

Backed by Experts

Benefit from a scheme backed by the European Investment Fund (EIF), European Investment Bank (EIB), and the Department of Environment, Climate and Communications (DECC).

Interest Rate: 4.2% (4.3% APRC)

The scheme benefits from a government funded interest rate subsidy of 2% which has been applied by NMCU and allows for a lower overall interest rate to be charged than other unsecured loan products.

Representative Example:

A loan of €50,000 at 4.2% variable interest rate (4.3% APRC*) repayable over 10 years would have 120 monthly repayments of €416.67.

Total cost of credit is €11,324.53. Total amount repayable is €61,324.53. Figures correct as at 31/03/2025.

How to apply

Step 1: Select one of the SEAI registered One Stop Shops or Community Project Co-ordinators to carry out an assessment of your residential property.

Step 2: Complete the assessment through your chosen SEAI registered One Stop Shop or Community Project Co-ordinator and you will receive a one-page Home Energy Summary Report.

Step 3: Apply for the loan. Enquire Online, or call us on 044 93 48817 to apply.

Please note: You will need to provide personal details along with supporting documents (including the Home Energy Summary Report) to complete the application, so please have this ready when starting the application. Approval of finance is subject to NMCU credit criteria, policies and procedures.

Applicants must utilise one of the above-mentioned service providers (SEAI registered One Stop Shop, Energy Partner, or Community Project Co-Ordinator) to carry out the energy efficiency upgrade works.

In addition, applicants must undertake the upgrade under one of the following SEAI grant programmes:

- National Home Energy Upgrade Scheme

- Better Energy Homes Scheme

- Community Energy Grant Scheme

Who can apply?

- A person that meets the eligibility criteria for the scheme

- See Eligibility Criteria section below

Who cannot apply?

- A person that does not meet the eligibility criteria for the scheme

- See Eligibility Criteria section below

Borrower Eligibility Criteria

- The applicant must be a natural person (meaning an individual, not a company) acting for his/her own benefit and not on behalf of someone else

- The applicant must not be a sanctioned person or in breach of certain restrictive measures

- The applicant must not be engaged in any illegal activities or illegal economic activities

- The applicant must not be tax resident in a non-compliant jurisdiction

- The applicant must not, to the best of his/her knowledge, be in an exclusion situation (including but not limited to being bankrupt, subject to insolvency proceedings, subject of a final judgment for fraud, corruption, participation in a criminal organisation, money laundering or terrorist financing, terrorist offences or human trafficking)

- The applicant must be able to provide confirmations in the scheme documentation, including that he/she will undertake the energy efficiency investment under the scheme on up to a maximum of three properties owned by him/her

- The applicant must be availing of a grant under a SEAI scheme for the purpose of funding (in part) the energy efficiency investment under the scheme

- The applicant must confirm ownership of an eligible property (see Eligible Property Criteria section below) by providing a self-declaration and the Meter Point Reference Number (MPRN) for the property

Loan Criteria

- The loan must be new

- The loan must be entered into by a finance provider during the relevant period

- The loan must be in the form of a term loan

- The loan must have a fixed repayment schedule providing for equal monthly instalments or equal monthly principal payments and must not include a period during which the principal is not payable

- The loan must be denominated in euro (EUR)

- The loan agreement must be valid, binding and enforceable under applicable law

- For loans issued with the specific purpose of financing the construction of new buildings and major rehabilitation of existing buildings, any such construction must comply with national energy standards (and certain additional requirements apply if loans are granted/issued with specific purpose of financing the heating and/or cooling of buildings)

- Loans with a “bullet repayment profile” (entire amount to be repaid at maturity) or “balloon” repayment profile (30% or more to be repaid at maturity) are not eligible under the scheme

- The proceeds of a loan must be applied towards the financing of eligible investment costs of an energy efficiency investment in accordance with the terms and conditions of a SEAI Scheme, and the energy efficiency investment must be carried out by a SEAI Project Intermediary

- The financing made available under the loan must not be used for refinancing of existing term loan debt, residential property renovation that has previously received other SEAI-funded grants for the same energy efficiency investment, and/or installation of any form of fossil fuel burners

- The minimum improvement in the energy performance of the property must be at least 20% when compared to the energy performance of the property before the energy efficiency investment commences

- The associated costs (if any) must make up a maximum of 30% of the eligible investment costs

- The loan must finance an energy efficiency investment carried out in compliance with minimum requirements with respect of environmental legislation and information access

- The proposed approved upgrade works costs, net of the proposed SEAI grant amount, must be at least 75% of the financing provided under the loan

- The actual upgrade works costs incurred under the loan, net of the actual SEAI grant amount, must be at least 70% of the financing provided under the loan

Eligible Property Criteria

- The property must be a residential property in the Republic of Ireland

- The property must not have been used in part for commercial purposes and in part for residential purposes at any time in previous 12 months, and the borrower must undertake not to use the property for such purposes for at least 12 months after they obtain finance

- The property must not have been subject to one or more short-term letting at any time in previous 12 months, and the borrower must undertake not to use the property for such purposes for at least 12 months after they obtain finance

- The property must not have been used as a holiday home at any time in previous 12 months, and the borrower must undertake not to use the property for such purposes for at least 12 months after they obtain finance

State Aid

The scheme will operate under the De Minimis Regulation.

State aid will apply on loans granted to any homeowner in which the underlying property (i) is currently being used; (ii) has been used in the previous 12 months; or (iii) will be used in the next 12 months for any rental or similar arrangement.

If the property/properties have been used for the above purposes, then there is “economic activity”, and State aid will arise on the grant of the loan(s) in respect of that property/properties.

Loans to other homeowners will not generate any State aid.

For a more extensive description of the State aid measures applicable to the scheme, please refer to the SBCI Regulation page.